A few years back, I started making enough money at my day job to have some savings left over after the basic monthly expenses like rent, food and commute were taken care of. Coincidentally, I also had to pay a significant amount in taxes for the first time around the same time.

Not having learnt a thing about managing money while at school, I took to books and YouTube channels authored by personal finance experts to figure out how to best manage my income, savings, and taxes.

This article is a summary of everything I've learnt and implemented in to practice since then. I've simplified and outlined the steps you'll need to take if you are in a similar station in life and wish to get an overall understanding of how to manage your money without needing a PhD in personal finance.

Table of Contents

The big idea

The goal is to organise and automate your finances so you only have to look at it once a year at most. Professional investors/traders can afford to put in all of their time into maximising their investment returns; however, this article is for those who do not wish to make a career out of this, and would rather invest their time in improving skills in their own area of expertise to maximise their earning potential.

Before we invest in equity, we need to secure ourselves from the volatility stocks bring - this is your holding power. When markets inevitably crash, this preparation will help you go through that economic downturn without much distress.

These ideas work best if:

- You are based in India (specific examples would be more relatable).

- Your primary source of income is a steady salary (a lot of the principles shared would still apply for those on irregular incomes).

- You have enough amount left over after paying for monthly expenses (if not, your focus should be on improving your Income or lowering your expenses).

Getting started: Managing cash flow

Most of us only have a single bank account. This muddies the waters. You should instead have the following 3 bank accounts to manage your cash flow.

- Income Account: All your income - salary, interest payments, and other sources of income are deposited into this bank account.

- Expense Account: Your monthly expenses (we'll discuss how to best calculate this a little later) is transferred into this bank account from your Income Account as soon as you receive your salary. Funds required to cover additional one time expenses specific to the upcoming month are also moved to the Expense Account from the income Account. All outgoing funds not intended for investments exit out of this account.

- Investment Account: All the money that remains in your Income Account after accounting for your next month's expense moves to this bank account. The only time money exits this account should be if it is intended for investments.

In addition to that, you should get yourself a credit card.

Preparation before you begin investing

In order to invest fearlessly and secure yourself from stock market's volatility, you first need to ensure that you're equipped to tackle any surprises life throws at you. Mainly, you need to protect yourself and your loved ones against loss of job, death, and medical emergencies.

Emergency Fund

An emergency fund's role is to cover your living expenses in the event that you lose your primary source of income until you are able to find a substitute.

Typically, it is advised for the emergency fund to be 6 to 12 times your monthly expenses.

For example: If you spend ₹50,000 per month to cover rent, food, and other living expenses, you should plan to have between ₹3,00,000 to ₹6,00,000 stored away. This money should be easily accessible at all times.

Term Insurance

The difference between a term insurance (also called Life Insurance) and a health insurance is that a life insurance pays a lump sum amount of money to the nominees in the event of your death, whereas a health insurance covers your hospitalisation costs.

You need a term insurance if you have dependents. For example, if your parents, wife or kids rely on you for financial support (either now or in the future), then you need a term insurance to secure their wellbeing in your absence.

As a rule of thumb, you need between 6 to 10 times your annual salary as the term insurance coverage.

Health Insurance

Now that you and your loved ones are secured against the possibility of you losing your job, or more unfortunately your life, it's time to sort out the last surprise expense that could eat away at your savings - hospitalisation - unless you plan for it's eventuality and purchase a robust health insurance.

There are plenty of options to choose from, and HDFC Ergo's Optima Restore plan is the most comprehensive (and also one of the most expensive) choices. This is the one I've opted in to. You'll also need a Top Up plan (this combo of a base plan plus a top up plan works better than going for a base plan with larger coverage).

Going into the details of how to pick a term and health insurance can become quite a lengthy topic, so I'll simply mention the conclusion of my findings and leave you to conduct further research if you're so inclined.

With that taken care of, you are now ready for investments in equity!

But first, a note on taxes.

Taxation

Depending on what income slab you fall under, you are taxed at a different percentage. Taxes aren't levied on your entire salary - there are certain expenses you'll make that are exempt from taxation. For example, if you make ₹5,00,000 per annum, and pay ₹2,00,000 in rent every year, then at this stage in the calculation, your taxable salary is ₹3,00,000. Similarly, there are certain investments that the government encourages, and will deduct your investment amount from the taxable salary so that your tax burden is smaller if you choose to opt into those investments.

Unless you have other obligations due to which you aren't able make these investments, it is advisable that you do so.

The government allows for ₹1,50,000 in annual deductions under 80C. This would include your term insurance and any Employee Provident Fund contributions you make (typically EPF is deducted from your salary before you receive it in-hand).

Term insurance and EPF alone won't account for the entire ₹1,50,000; so you can invest the rest of the amount in Personal Provident Fund, or an ELSS mutual fund (PPF is safer than ELSS, but ELSS provides higher returns - if you accept the greater risk). Both PPF and ELSS are tax-saving investments.

Under 80D, your health insurance expenses are exempted.

Investing

You'll need to understand a few basics about investing to help you get started.

The Fundamentals

Debt vs Equity

Risk and Reward are directly proportional to each other when it comes to investing. The more appetite you have to take risks, the higher is your potential rate of return. For instance: An investment in debt is known to be a relatively safe investment option, with returns that are lower than investments in equity as equity is known to come with greater risks.

Goals and Horizon

For any amount of money you invest, you need to have a time horizon in mind - which depends on your intention for investing, or in other words, your goal. For instance, if you wish to invest ₹1,00,000 today because you wish to save this money to cover a vacation expense due next year, your horizon for this investment is 1 year. However, if you wish to invest that same amount to cover your retirement expenses, your horizon for this investment would be however many years you are away from retiring. What investment option is right for you will depend on your horizon, which depends on your goals. Typically, debt investments are preferred for short term goals, and equity is suited to investments with at least a 5 to 7 year horizon.

How your age affects your investment strategy

Because equity investments are volatile in the short term (less than 5 to 7 years), it isn't suited to someone who is near retirement. On the other hand, someone much younger can wait out a turbulence in the stock market (especially if they have an emergency fund and insurances set up) and take advantage of its higher average rate of return.

The rule of thumb is to reserve as much percentage split in debt as your age. For instance, if you are 30 years old, you'd invest 30% of your funds in debt, and 70% in equity. As you grow older, this split will start leaning heavier towards debt so that by the time you're near retirement, most of your funds are in the relatively safer and less turbulent debt type investments.

Large Cap, Mid Cap, and Small Cap

The equity/stock market can be broken down into 3 segments:

Large-cap companies are businesses that are well-established and have a significant market share. Large-cap companies have market caps of Rs 20,000 crore or more. Within equity, investments in Large Cap are understood to be the safest option.

Mid-cap companies are companies whose market cap is above Rs 5,000 crore but less than Rs 20,000 crore. Investing in these companies can be riskier than investing in large-cap market companies. This is because mid-caps tend to be more volatile.

Small-cap companies are those that have a market capitalisation of less than Rs 5,000 crore. These companies are relatively smaller in size and have significant growth potential. As we have learnt so far, with high rewards come higher risks.

Direct vs Regular Mutual Funds

Mutual funds can either be purchased directly from the AMC (direct mutual funds), or via a third party broker (regular mutual funds). When it comes to a fund with the same name - and the only difference being between one being regular and the other bring direct - always opt for the direct option. In fact, as a rule of thumb, never opt for a Regular Mutual Fund. You are paying commission to a third party for as long as you hold that fund, and for no good reason as it's fairly straightforward to purchase direct from the AMC and save this cost.

Debt Investing

I would recommend the following two debt investments.

Employees’ Provident Fund

In case you are eligible for Employees' Provident Fund (EPF), a certain percentage of your basic salary can be invested in EPF. In my case, my employer deducts the company’s share as well as my share of the EPF contribution from my salary and makes this investment on my behalf.

Last year, EPF’s rate of return was 8.5% (this is adjusted every year). This is quite a decent return for a debt type investment.

Public Provident Fund

I would suggest you go ahead and open up a Public Provident Fund (PPF) account regardless of if you wish to make immediate use of it. A PPF account holder can fully withdraw the account balance only upon the scheme's maturity i.e., post the completion of 15 years. Opening up the PPF account starts this countdown of 15 years so that even if you begin investing in PPF after a few years, you don’t have to wait another 15 years starting from that time. In order to maintain an active PPF account, a minimum annual investment of ₹500 is necessary.

Between EPF and PPF, the debt component of your investment portfolio should be satisfied.

Equity Investing

Everything we have discussed so far has been in preparation for investments in equity! Over a long enough duration, equity investments in India can be expected to deliver an average of 12% annual rate of return.

I invest all my money via Mutual Funds.

Equity Linked Savings Schemes (ELSS)

ELSS funds are a special type of mutual funds which help save tax. So, invest as much as you need to every month via SIPs (more on this later) to get maximum tax deductions via Section 80C, but no more! One downside to ELSS funds is that it comes with a 3 year lock-in period - meaning you can’t withdraw your funds until the amount has spent at least 3 years in the fund. Invest as much as you need to to save on tax, and save the rest for other Mutual Funds.

My preferred ELSS fund to invest in is Axis Long Term Equity Fund Direct Plan Growth Option.

Mutual Fund Investing

Outside of ELSS, I have investments in 5 other mutual funds. Here is a breakdown of how much I invest every month in each of my mutual funds:

Fund Name | Allocation |

25% | |

Axis Midcap Fund Direct Plan Growth | 21% |

Parag Parikh Flexi Cap Direct Growth | 18% |

UTI Nifty Index Fund-Growth Option- Direct | 16% |

Nippon India Small Cap Fund - Direct Plan - Growth Plan | 12% |

Motilal Oswal S&P 500 Index Fund Direct Growth | 8% |

We’ve already understood why to invest in ELSS and how much; to get a grasp of why these other 5 funds were picked, let’s take a quick look at what each of these brings to the table:

- Axis Midcap Fund Direct Plan Growth: This fund provides exposure to Midcap companies.

- Parag Parikh Flexi Cap Direct Growth: This fund invests in foreign equities, which further diversifies your portfolio.

- UTI Nifty Index Fund: This fund increases my exposure to Large Cap funds. As it doesn’t come with a lock-in period, I prefer investing here instead of increasing my investment in ELSS to meet the same goal.

- Nippon India Small Cap Fund: This fund is to include a Small Cap portion to my portfolio.

- Motilal Oswal S&P 500 Index Fund: The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the performance of 500 large companies listed on stock exchanges in the United States. It is one of the most commonly followed equity indices. Motilal Oswal S&P 500 Index Fund tracks/mimics the S&P 500 Index.

How to pick these Mutual Funds:

You could either watch a few dozen YouTube videos to understand how to pick the best Mutual Funds, or outsource this task to a trusted partner at a small fee. There are 2 types of Financial Advisors: Those who work on commission, and those who provide a fixed service (like a one time portfolio planning) at a fixed cost. The second type of financial advisors are preferable as they do not have any motivation to promote a specific fund over another for their own gains.

Outside of these 2 options, you could consult with experts on an app like INDmoney. INDmoney makes their money via users’ subscriptions, and not by commissions. This is one reason why I trust their advise.

You can sign up for a month to their paid plan and get their recommendation on how to pick the right mutual funds for your specific situation. You could have a well thought out portfolio in less than a few days with this shortcut.

Gold Investing

Gold is inversely correlated with the stock market and could do well during an economic slump. You should have about 10% of your portfolio in Gold.

There are many ways to invest in Gold - purchasing actual gold is perhaps the least efficient way. You should instead invest in Gold via Sovereign Gold Bonds.

The current interest rate for SGB is 2.50% per annum on your initial investment. It is paid twice a year (semi-annually). In addition to this interest, returns are usually linked to the current market price of gold. Therefore the real rate of return on Sovereign gold bond is around 10% per annum.

The tenure of SGBs is eight years. The Sovereign Gold Bonds in India have a mandatory lock-in period of five years.

Managing your money

My money philosophy

At this point you've secured yourself against loss of job, health, and life; taken care of your monthly expenses, and invested the rest of the money. This is a strategy that works great when you are building up your net worth from nothing to something that gives you a fair bit of mental peace. At the end of the day, that's what this is all about: Making sure you have enough mental peace with regards to money so that you can enjoy life to the fullest.

Once I had built up enough net worth, I found this strategy to be limiting. It set me up for a successful future but left nothing for the present apart from monthly expenses and a few planned holidays.

To address this concern, I briefly stopped investing to redirect all that money to solving some of life's pressing issues. I re-did my wardrobe, fixed my teeth with an Invisalign treatment, and decided to take a comfortable cab to work every day instead of public transport so I can make better use of those hours.

Focusing intensely on building my net worth and then solely on improving life in the moment are both extremes, ones I needed to experience so I can come to appreciate need for the balance.

To maintain a balance, I've now decided to cap my investments to about 20% of my salary instead of the entire amount that's left over after monthly expenses. With this reduced investment obligation, I can divert the remaining money towards improving my knowledge, skills, and dating life in the months to come.

To better plan for this investment-in-self, I set up a few spreadsheets. You can find links to them in the following section (these sheets are filled in with dummy values you can modify to better reflect your situation). Feel free to make a copy and use them to your benefit.

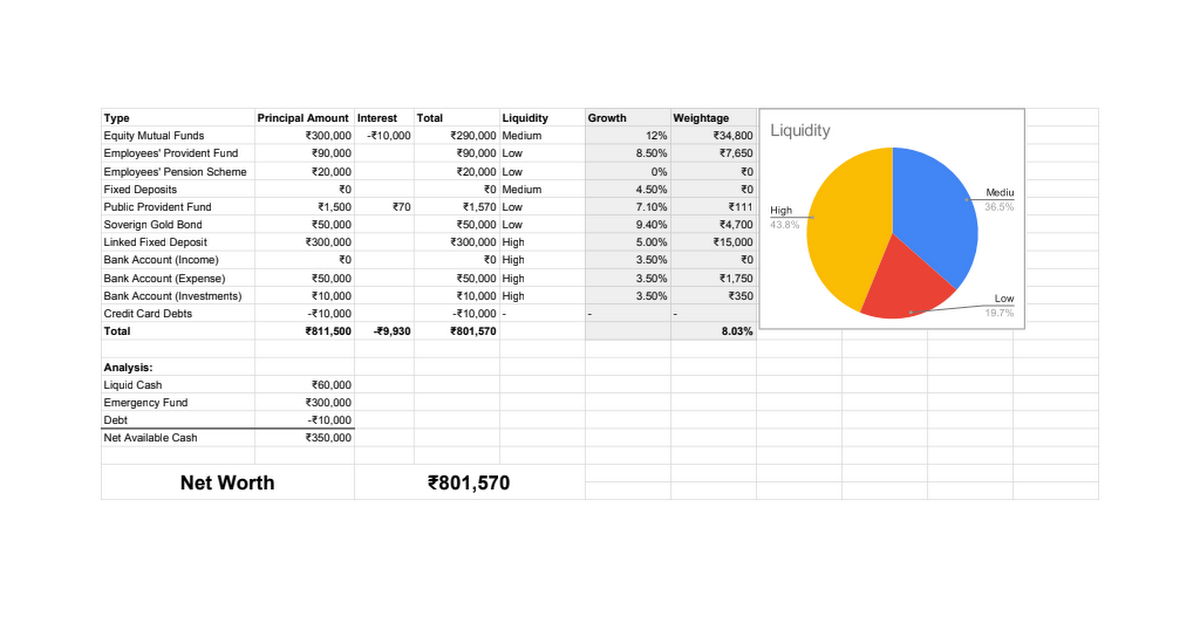

Net worth calculator

Your current net worth is the sum of all your investments, interest generated, emergency fund, and bank balance subtracted by any debts you owe (credit cards, loans, EMIs etc.).

Feel free to make a copy of this Google Sheet with dummy data and tweak it to your specific circumstances.

Recurring Expense Tracking

All your predictable recurring monthly expenses can be listed on this Monthly Expense Tracker. We’ll use this knowledge to calculate your disposable income in the next step.

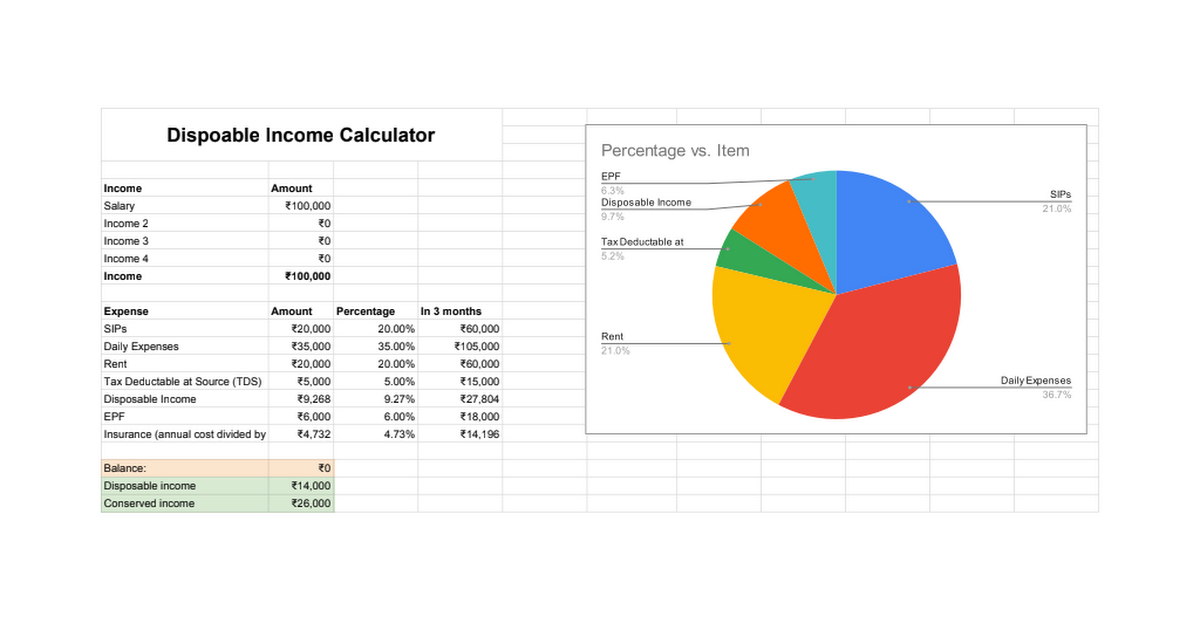

Disposable income calculator

Calculating your disposable income helps you determine what amount is left over month on month after every predictable and recurring expense as well as your investment goals are taken care of. This is the remaining amount which will fund your passion project, your travel, and any other goals you may have.

This Google Sheet helps you calculate your disposable and conserved income.

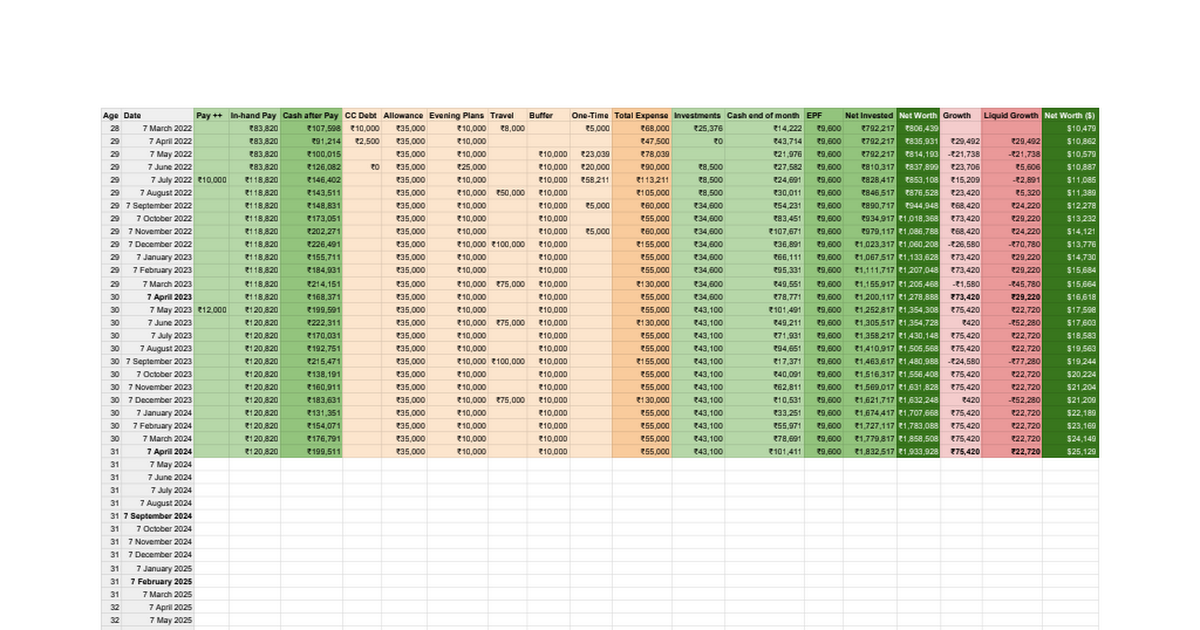

Projections

This projections sheet takes into consideration other one-time expenses outside of your predictable ones, and shows how much you are going to have in the bank at the end of each month after you’ve budgeted for all your plans, hopes, and dreams. This is the money you use to find even larger goals.

Other thoughts

- Crypto investments: We should only invest our money in things we understand; and I am yet to understand the intrinsic value of cryptocurrencies. I’ll reserve my decision on if or not to invest in it until I’ve conducted further research.

- The sooner you purchase the term insurance, the better it is. Premiums are lower when you're younger, and stay the same year-on-year. So lock in that lower-priced premium early on.

Resources

- Personal Finance book by Monika Halan: Let’s talk money.

- The Psychology of Money by Morgan Housel.